lo.95 hi.80 hi.95

## <date> <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 2010-01-01 actual 6558 NA NA NA NA

## 2 2010-02-01 actual 7481 NA NA NA NA

## 3 2010-03-01 actual 9475 NA NA NA NA

## 4 2010-04-01 actual 9424 NA NA NA NA

## 5 2010-05-01 actual 9351 NA NA NA NA

## 6 2010-06-01 actual 10552 NA NA NA NA

## 7 2010-07-01 actual 9077 NA NA NA NA

## 8 2010-08-01 actual 9273 NA NA NA NA

## 9 2010-09-01 actual 9420 NA NA NA NA

## 10 2010-10-01 actual 9413 NA NA NA NA

## # ... with 86 more rows

STEP 5:比较真实值和预测值

我们可以使用 tq_get() 来检索实际数据。注意,我们没有用于比较的完整数据,但我们至少可以比较前几个月的实际值。

actuals_tbl <- tq_get(

"S4248SM144NCEN",

get = "economic.data",

from = "2017-01-01",

to = "2017-12-31")

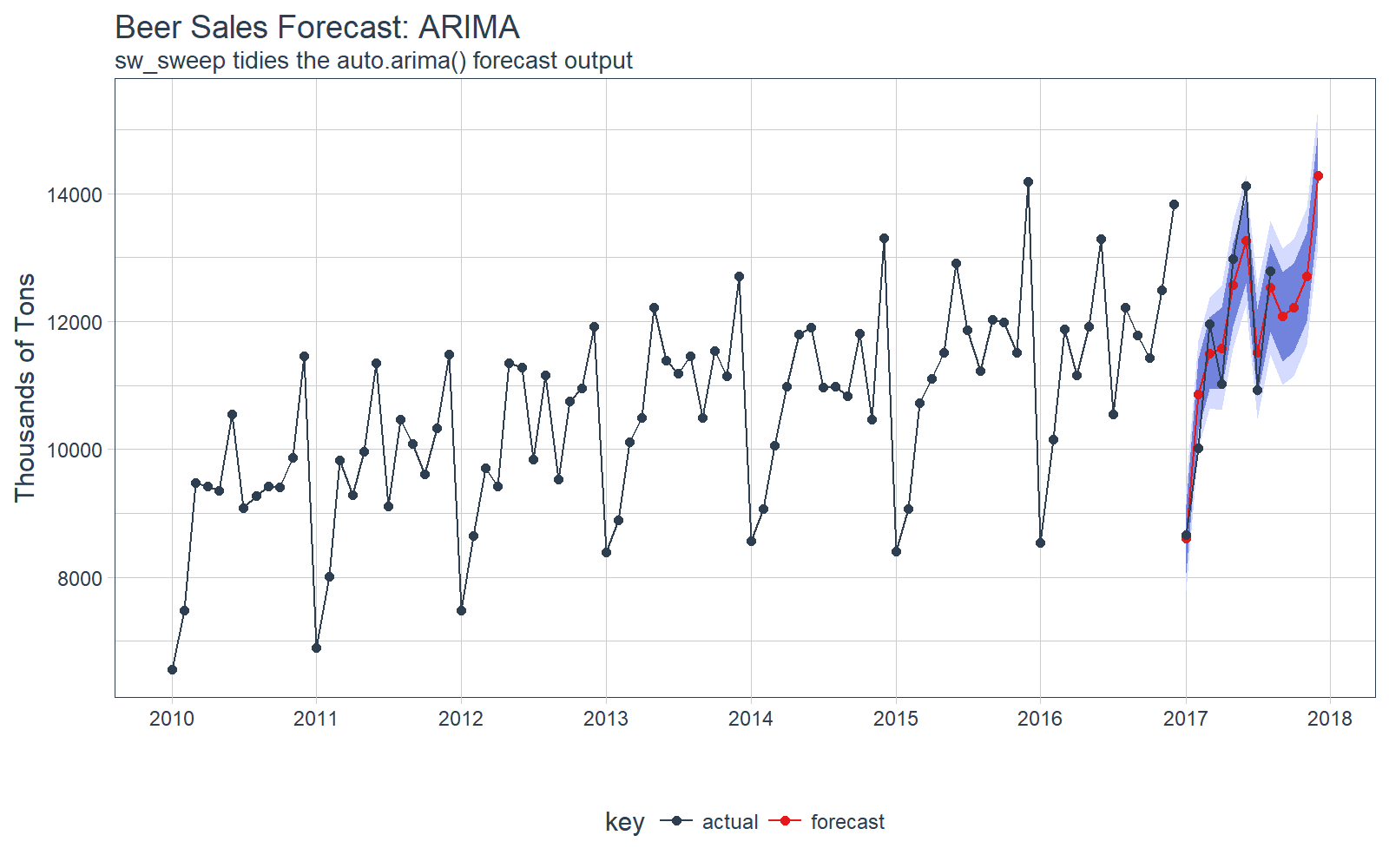

注意,预测结果放在 tibble 中,可以方便的实现可视化。

# Visualize the forecast with ggplot

fcast_tbl %>%

ggplot(

aes(x = index, y = price, color = key)) +

# 95% CI

geom_ribbon(

aes(ymin = lo.95, ymax = hi.95),

fill = "#D5DBFF", color = NA, size = 0) +

# 80% CI

geom_ribbon(

aes(ymin = lo.80, ymax = hi.80, fill = key),

fill = "#596DD5", color = NA,

size = 0, alpha = 0.8) +

# Prediction

geom_line() +

geom_point() +

# Actuals

geom_line(

aes(x = date, y = price), color = palette_light()[[1]],

data = actuals_tbl) +

geom_point(

aes(x = date, y = price), color = palette_light()[[1]],

data = actuals_tbl) +

# Aesthetics

labs(

title = "Beer Sales Forecast: ARIMA", x = "", y = "Thousands of Tons",

subtitle = "sw_sweep tidies the auto.arima() forecast output") +

scale_x_date(

date_breaks = "1 year",

date_labels = "%Y") +

scale_color_tq() +

scale_fill_tq() +

theme_tq()

我们可以研究测试集上的误差(真实值 vs 预测值)。

# Investigate test error

error_tbl <- left_join(

actuals_tbl,

fcast_tbl,

by = c("date" = "index")) %>%

rename(

actual = price.x, pred = price.y) %>%

select(date, actual, pred) %>%

mutate(

error = actual - pred,

error_pct = error / actual)

error_tbl

## # A tibble: 8 x 5

## date actual pred error error_pct

## <date> <int> <dbl> <dbl> <dbl>

## 1 2017-01-01 8664 8601.815 62.18469 0.007177365

## 2 2017-02-01 10017 10855.429 -838.42908 -0.083700617

## 3 2017-03-01 11960 11502.214 457.78622 0.038276439

## 4 2017-04-01 11019 11582.600 -563.59962 -0.051147982

## 5 2017-05-01 12971 12566.765 404.23491 0.031164514

## 6 2017-06-01 14113 13263.918 849.08191 0.060163106

## 7 2017-07-01 10928 11507.277 -579.27693 -0.053008504

## 8 2017-08-01 12788 12527.278 260.72219 0.020388035

并且,我们可以做简单的误差度量。MAPE 接近 4.3%,比简单的线性回归模型略好一点,但是 RMSE 变差了。

# Calculate test error metrics

test_residuals <- error_tbl$error

test_error_pct <- error_tbl$error_pct * 100 # Percentage error

me <- mean(test_residuals, na.rm=TRUE)

rmse <- mean(test_residuals^2, na.rm=TRUE)^0.5

mae <- mean(abs(test_residuals), na.rm=TRUE)

mape <- mean(abs(test_error_pct), na.rm=TRUE)

mpe <- mean(test_error_pct, na.rm=TRUE)

tibble(me, rmse, mae, mape, mpe) %>%

glimpse()

## Observations: 1

## Variables: 5

## $ me <dbl> 6.588034

## $ rmse <dbl> 561.4631

## $ mae <dbl> 501.9144

## $ mape <dbl> 4.312832

## $ mpe <dbl> -0.3835956