rdized Root Mean Square Residual:

SRMR 0.065

#以下是参数估计部分

Parameter Estimates:

Information Expected

Standard Errors Standard

Latent Variables:

Estimate Std.Err z-value P(>|z|)

visual =~

x1 1.000

x2 0.554 0.100 5.554 0.000

x3 0.729 0.109 6.685 0.000

textual =~

x4 1.000

x5 1.113 0.065 17.014 0.000

x6 0.926 0.055 16.703 0.000

speed =~

x7 1.000

x8 1.180 0.165 7.152 0.000

x9 1.082 0.151 7.155 0.000

Covariances:

Estimate Std.Err z-value P(>|z|)

visual ~~

textual 0.408 0.074 5.552 0.000

speed 0.262 0.056 4.660 0.000

textual ~~

speed 0.173 0.049 3.518 0.000

Variances:

Estimate Std.Err z-value P(>|z|)

.x1 0.549 0.114 4.833 0.000

.x2 1.134 0.102 11.146 0.000

.x3 0.844 0.091 9.317 0.000

.x4 0.371 0.048 7.779 0.000

.x5 0.446 0.058 7.642 0.000

.x6 0.356 0.043 8.277 0.000

.x7 0.799 0.081 9.823 0.000

.x8 0.488 0.074 6.573 0.000

.x9 0.566 0.071 8.003 0.000

visual 0.809 0.145 5.564 0.000

textual 0.979 0.112 8.737 0.000

speed 0.384 0.086 4.451 0.000

例1是一个定义模型、拟合模型、提取结果的过程。

5. 例2:结构方程(SEM)

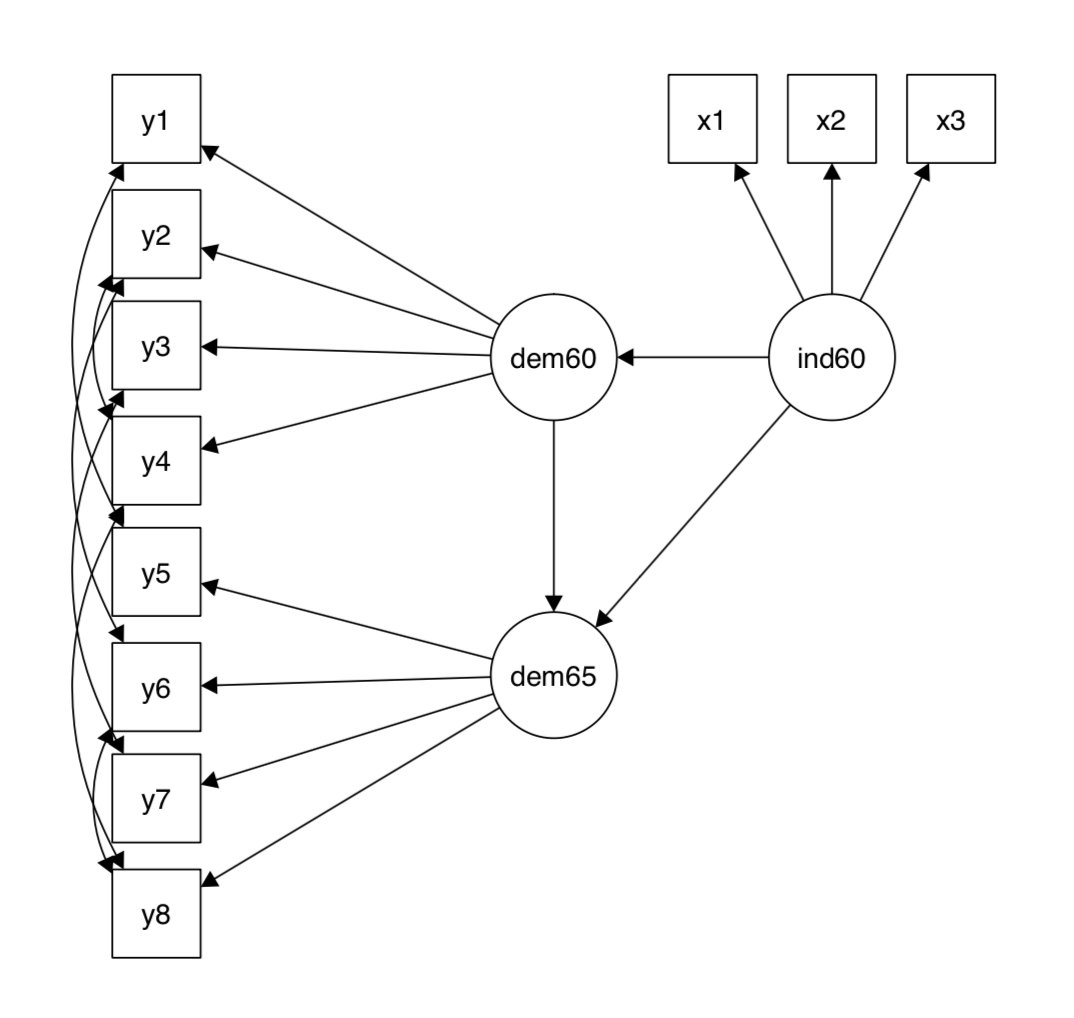

例2中我们使用名为PoliticalDemocracy的数据集,图示如下:

数据形式大致如下(只显示前三行):

| ind60 |

1960年的非民主情况 |

y5 |

1965年专家对出版物自由的评价 |

| dem60 |

1960年的民主情况 |

y6 |

1965年的反对党派自由 |

| dem65 |

1965年的民主情况 |

y7 |

1965年选举的公平性 |

| y1 |

1960年专家对出版物自由的评价 |

y8 |

1965年选举产生的立法机关效率 |

| y2 |

1960年的反对党派自由 |

x1 |

1960年每单位资本GNP |

| y3 |

1960年选举的公平性 |

x2 |

1960年每单位资本的物质能量消费 |

| y4 |

1960年选举产生的立法机关效率 |

x3 |

1960年工业劳动力占比 |

模型如下:

model <- '# measurement model 测量模型

ind60 =~ x1 + x2 + x3

dem60 =~ y1 + y2 + y3 + y4

dem65 =~ y5 + y6 + y7 + y8

# regressions 回归

dem60 ~ ind60

dem65 ~ ind60 + dem60

# residual correlations 残余相关

y1 ~~ y5

y2 ~~ y4 + y6

y3 ~~ y7

y4 ~~ y8

y6 ~~ y8'

# 拟合SEM

fit <- sem(model, data = PoliticalDemocracy)

# 提取结果

summary(fit, standardized = TRUE)

#与上例不同,这里我们忽略了参数fit.measure = TRUE,用standardized = TRUE来标准化参数值)

结果如下:

lavaan (0.5-23.1097) converged normally after 68 iterations

Number of observations 75

Estimator ML

Minimum Function Test Statistic 38.125

Degrees of freedom 35

P-value (Chi-square) 0.329

Parameter Estimates:

Information Expected

Standard Errors Standard

Latent Variables:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

ind60 =~

x1 1.000 0.670 0.920

x2 2.180 0.139 15.742 0.000 1.460 0.973

x3 1.819 0.152 11.967 0.000 1.218 0.872

dem60 =~

y1 1.000 2.223 0.850

y2 1.257 0.182 6.889 0.000 2.794 0.717

y3 1.058 0.151 6.987 0.000 2.351 0.722

y4 1.265 0.145 8.722 0.000 2.812 0.846

dem65 =~

y5 1.000 2.103 0.808

y6 1.186 0.169 7.024 0.000 2.493 0.746

y7 1.280 0.160 8.002 0.000 2.691 0.824

y8 1.266 0.158 8.007 0.000 2.662 0.828

Regressions:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

dem60 ~

ind60 1.483 0.399 3.715 0.000 0.447 0.447

dem65 ~

ind60 0.572 0.221 2.586 0.010 0.182 0.182

dem60 0.837 0.098 8.514 0.000 0.885 0.885

Covariances:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

.y1 ~~

.y5 0.624 0.358 1.741 0.082 0.624 0.296

.y2 ~~

.y4 1.313 0.702 1.871 0.061 1.313 0.273

.y6 2.153 0.734 2.934 0.003 2.153 0.356

.y3 ~~

.y7 0.795 0.608 1.308 0.191 0.795 0.191

.y4 ~~

.y8 0.348 0.442 0.787 0.431 0.348 0.109

.y6 ~~

.y8 1.356 0.568 2.386 0.017 1.356 0.338

Variances:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

.x1 0.082 0.019 4.184 0.000 0.082 0.154

.x2 0.120 0.070 1.718 0.086 0.120 0.053

.x3 0.467 0.090 5.177 0.000 0.467 0.239

.y1 1.891 0.444 4.256 0.000 1.891 0.277

.y2 7.373 1.374 5.366 0.000 7.373 0.486

.y3 5.067 0.952 5.324 0.000 5.067 0.478

.y4 3.148 0.739 4.261 0.000 3.148 0.28