t_arr, batch_size = batch_size) %>%

.[,1]

# Retransform values

pred_tbl <- tibble(

index = lag_test_tbl$index,

value = (pred_out * scale_history + center_history)^2)

# Combine actual data with predictions

tbl_1 <- df_trn %>%

add_column(key = "actual")

tbl_2 <- df_tst %>%

add_column(key = "actual")

tbl_3 <- pred_tbl %>%

add_column(key = "predict")

# Create time_bind_rows() to solve dplyr issue

time_bind_rows <- function(data_1, data_2, index) {

index_expr <- enquo(index)

bind_rows(data_1, data_2) %>%

as_tbl_time(index = !! index_expr)

}

ret <- list(tbl_1, tbl_2, tbl_3) %>%

reduce(time_bind_rows, index = index) %>%

arrange(key, index) %>%

mutate(key = as_factor(key))

return(ret)

}

safe_lstm <- possibly(lstm_prediction, otherwise = NA)

safe_lstm(split, epochs, ...)

}

我们测试下 predict_keras_lstm() 函数,设置 epochs = 10。返回的数据为长格式,在 key 列中标记有 actual 和 predict。

predict_keras_lstm(split, epochs = 10)

## # A time tibble: 840 x 3

## # Index: index

## index value key

## <date> <dbl> <fct>

## 1 1949-11-01 144. actual

## 2 1949-12-01 118. actual

## 3 1950-01-01 102. actual

## 4 1950-02-01 94.8 actual

## 5 1950-03-01 110. actual

## 6 1950-04-01 113. actual

## 7 1950-05-01 106. actual

## 8 1950-06-01 83.6 actual

## 9 1950-07-01 91.0 actual

## 10 1950-08-01 85.2 actual

## # ... with 830 more rows

5.2.2 将 LSTM 预测函数应用到 11 个样本上

既然 predict_keras_lstm() 函数可以在一个样本上运行,我们现在可以借助使用 mutate() 和 map() 将函数应用到所有样本上。预测将存储在名为 predict 的列中。注意,这可能需要 5-10 分钟左右才能完成。

sample_predictions_lstm_tbl <- rolling_origin_resamples %>%

mutate(predict = map(splits, predict_keras_lstm, epochs = 300))

现在,我们得到了 11 个样本的预测,数据存储在列 predict 中。

sample_predictions_lstm_tbl

## # Rolling origin forecast resampling

## # A tibble: 11 x 3

## splits id predict

## * <list> <chr> <list>

## 1 <S3: rsplit> Slice01 <tibble [840 x 3]>

## 2 <S3: rsplit> Slice02 <tibble [840 x 3]>

## 3 <S3: rsplit> Slice03 <tibble [840 x 3]>

## 4 <S3: rsplit> Slice04 <tibble [840 x 3]>

## 5 <S3: rsplit> Slice05 <tibble [840 x 3]>

## 6 <S3: rsplit> Slice06 <tibble [840 x 3]>

## 7 <S3: rsplit> Slice07 <tibble [840 x 3]>

## 8 <S3: rsplit> Slice08 <tibble [840 x 3]>

## 9 <S3: rsplit> Slice09 <tibble [840 x 3]>

## 10 <S3: rsplit> Slice10 <tibble [840 x 3]>

## 11 <S3: rsplit> Slice11 <tibble [840 x 3]>

5.2.3 评估回测表现

通过将 calc_rmse() 函数应用到 predict 列上,我们可以得到所有样本的 RMSE。

sample_rmse_tbl <- sample_predictions_lstm_tbl %>%

mutate(rmse = map_dbl(predict, calc_rmse)) %>%

select(id, rmse)

sample_rmse_tbl

## # Rolling origin forecast resampling

## # A tibble: 11 x 2

## id rmse

## * <chr> <dbl>

## 1 Slice01 48.2

## 2 Slice02 17.4

## 3 Slice03 41.0

## 4 Slice04 26.6

## 5 Slice05 22.2

## 6 Slice06 49.0

## 7 Slice07 18.1

## 8 Slice08 54.9

## 9 Slice09 28.0

## 10 Slice10 38.4

## 11 Slice11 34.2

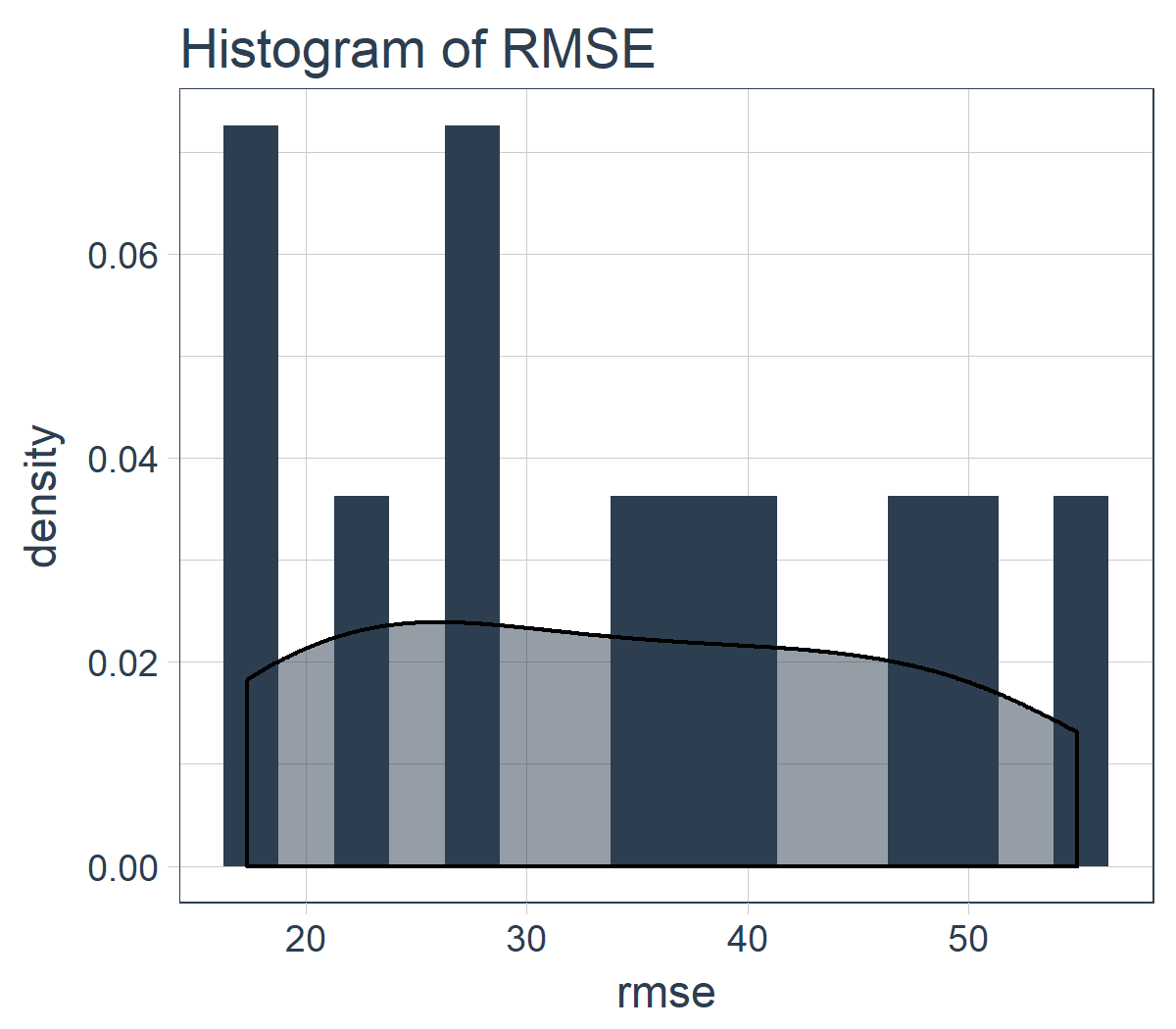

sample_rmse_tbl %>%

ggplot(aes(rmse)) +

geom_histogram(

aes(y = ..density..),

fill = palette_light()[[1]], bins = 16) +

geom_density(

fill = palette_light()[[1]], alpha = 0.5) +

theme_tq() +

ggtitle("Histogram of RMSE")

而且,我们可以总结 11 个样本的 RMSE。专业提示:使用 RMSE(或其他类似指标)的平均值和标准差是比较各种模型表现的好方法。

sample_rmse_tbl %>%

summarize(

mean_rmse = mean(rmse),

sd_r