面我们就要建立 ARIMA 模型了。

STEP 2A:ARIMA 模型

我们使用 forecast 包里的 auto.arima() 函数为时间序列建模。

# Model using auto.arima

fit_arima <- auto.arima(beer_sales_ts)

fit_arima

## Series: beer_sales_ts

## ARIMA(3,0,0)(1,1,0)[12] with drift

##

## Coefficients:

## ar1 ar2 ar3 sar1 drift

## -0.2498 0.1079 0.6210 -0.2817 32.1157

## s.e. 0.0933 0.0982 0.0925 0.1333 5.8882

##

## sigma^2 estimated as 175282: log likelihood=-535.49

## AIC=1082.97 AICc=1084.27 BIC=1096.63

STEP 2B:简化模型

就像 broom 简化 stats 包的使用一样,我么可以使用 sweep 的函数简化 ARIMA 模型。下面介绍三个函数:

sw_tidy():用于检索模型参数sw_glance():用于检索模型描述和训练集的精确度度量sw_augment():用于获得模型残差

sw_tidy

sw_tidy() 函数以 tibble 对象的形式返回模型参数。

# sw_tidy - Get model coefficients

sw_tidy(fit_arima)

## # A tibble: 5 x 2

## term estimate

## <chr> <dbl>

## 1 ar1 -0.2497937

## 2 ar2 0.1079269

## 3 ar3 0.6210345

## 4 sar1 -0.2816877

## 5 drift 32.1157478

sw_glance

sw_glance() 函数以 tibble 对象的形式返回训练集的精确度度量。可以使用 glimpse 函数美化显示结果。

# sw_glance - Get model description and training set accuracy measures

sw_glance(fit_arima) %>%

glimpse()

## Observations: 1

## Variables: 12

## $ model.desc <chr> "ARIMA(3,0,0)(1,1,0)[12] with drift"

## $ sigma <dbl> 418.6665

## $ logLik <dbl> -535.4873

## $ AIC <dbl> 1082.975

## $ BIC <dbl> 1096.635

## $ ME <dbl> 1.189875

## $ RMSE <dbl> 373.9091

## $ MAE <dbl> 271.7068

## $ MPE <dbl> -0.06716239

## $ MAPE <dbl> 2.526077

## $ MASE <dbl> 0.4989005

## $ ACF1 <dbl> 0.02215405

sw_augument

sw_augument() 函数返回的 tibble 表中包含 .actual、.fitted 和 .resid 列,有助于在训练集上评估模型表现。注意,设置 timetk_idx = TRUE 返回初始的日期索引。

# sw_augment - get model residuals

sw_augment(fit_arima, timetk_idx = TRUE)

## # A tibble: 84 x 4

## index .actual .fitted .resid

## <date> <dbl> <dbl> <dbl>

## 1 2010-01-01 6558 6551.474 6.525878

## 2 2010-02-01 7481 7473.583 7.416765

## 3 2010-03-01 9475 9465.621 9.378648

## 4 2010-04-01 9424 9414.704 9.295526

## 5 2010-05-01 9351 9341.810 9.190414

## 6 2010-06-01 10552 10541.641 10.359293

## 7 2010-07-01 9077 9068.148 8.852178

## 8 2010-08-01 9273 9263.984 9.016063

## 9 2010-09-01 9420 9410.869 9.130943

## 10 2010-10-01 9413 9403.908 9.091831

## # ... with 74 more rows

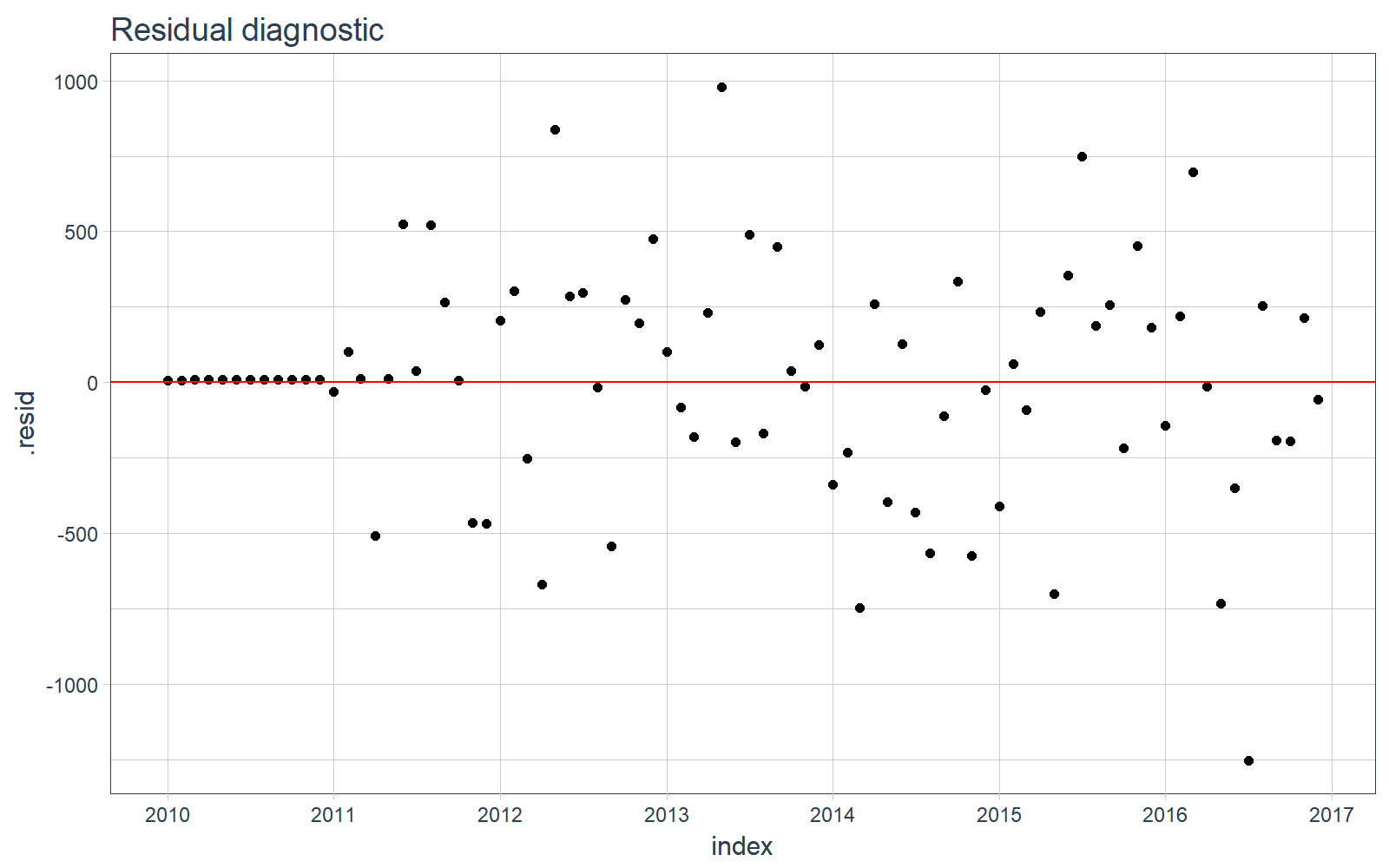

我们可以可视化训练数据上的残差,看一下数据中有没有遗漏的模式没有被发现。

# Plotting residuals

sw_augment(fit_arima, timetk_idx = TRUE) %>%

ggplot(aes(x = index, y = .resid)) +

geom_point() +

geom_hline(yintercept = 0, color = "red") +

labs(title = "Residual diagnostic") +

scale_x_date(date_breaks = "1 year", date_labels = "%Y") +

theme_tq()

STEP 3:预测

使用 forecast() 函数做预测。

# Forecast next 12 months

fcast_arima <- forecast(fit_arima, h = 12)

一个问题是,预测结果并不“tidy”。我们需要数据框形式的预测结果,以便应用 tidyverse 的功能,然而预测结果是 forecast 类型的,一种基于 ts 的对象。

class(fcast_arima)

## [1] "forecast"

STEP 4:用 sweep 简化预测

我们使用 sw_sweep() 简化预测结果,一个额外的好处是,如果 forecast 对象有 timetk 索引,我们可以用它返回一个日期时间索引,不同于 ts 对象的规则索引。

首先要确认 forecast 对象有 timetk 索引,这需要在使用 sw_sweep() 时设置 timetk_idx 参数。

# Check if object has timetk index

has_timetk_idx(fcast_arima)

## [1] TRUE

现在,使用 sw_sweep() 来简化预测结果,它会在内部根据 time_tk 构造一条未来时间序列索引(这一步总是会被执行,因为我们在第 1 步中用 tk_ts() 构造了 ts 对象)注意:这意味着我们最终可以在 forecast 包中使用日期(不同于 ts 对象中的规则索引)!。

# sw_sweep - tidies forecast output

fcast_tbl <- sw_sweep(fcast_arima, timetk_idx = TRUE)

fcast_tbl

## # A tibble: 96 x 7

## index key price lo.80